At Netflix, A Few Hits Subsidize Many Misses

Netflix is a fascinating case study in high volume and high variance. By now, it’s no secret that the market-leading streaming company releases more original product than any other competitor. Even as Netflix (and the industry as a whole) reduces its regular output amid a production contraction, audiences can still expect a healthy diet of fresh material from the service. After all, the more lottery tickets you buy, the greater the chance of hitting the jackpot, right?

Yes and no.

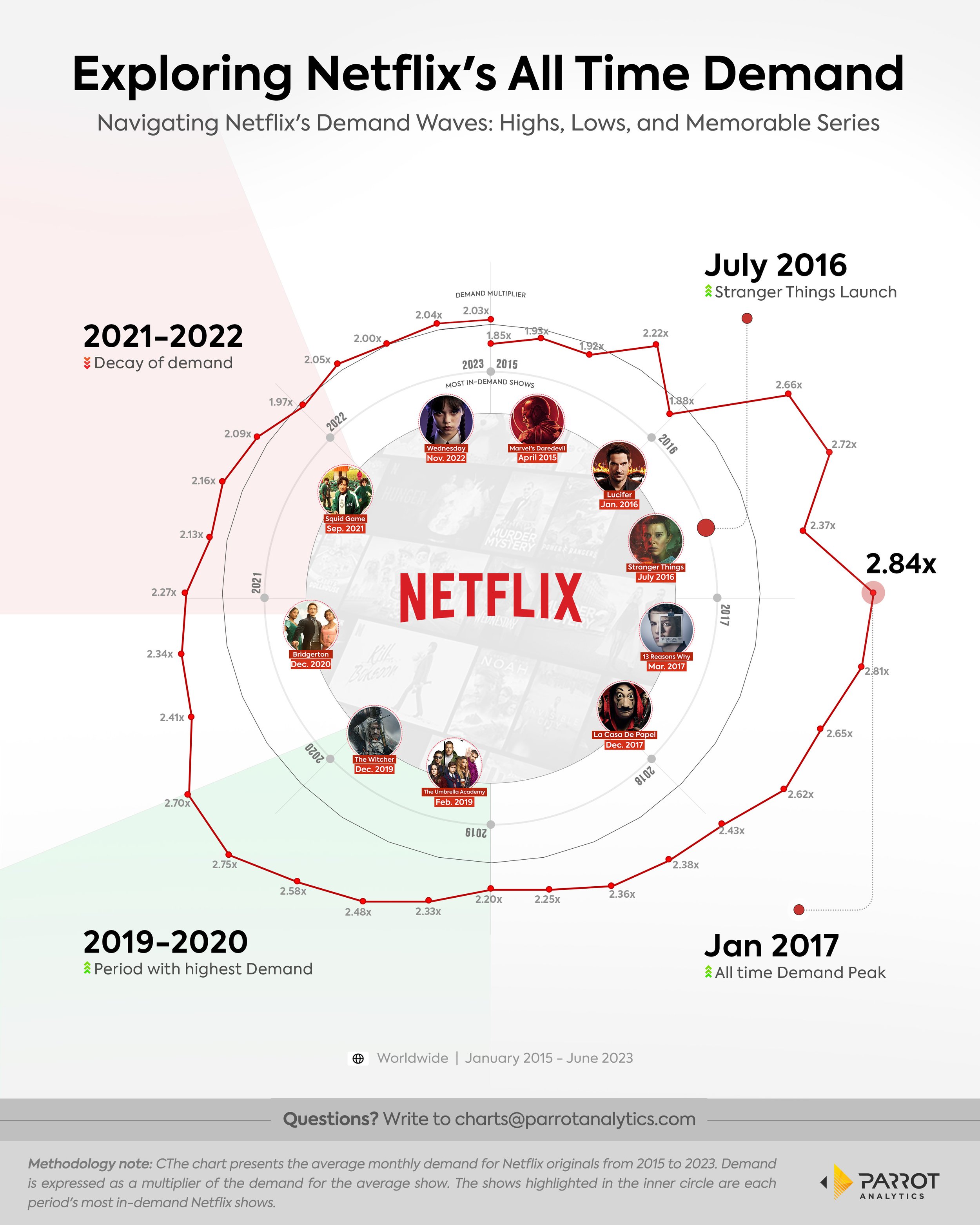

This graph from Parrot Analytics looks at the average audience demand for all Netflix shows since 2015. Of course, the most well-known and popular series enjoy higher demand levels, but the majority of shows fail to resonate (one reason why streamers have fought against transparency is to conceal this very fact from Wall Street). So, for every Stranger Things and Squid Game that emerges as a breakout broad appeal hit, there are numerous forgettable misses that generate demand levels around 1x or lower.

You’ll notice the inner circle of the graph is dotted with some of Netflix’s most in-demand originals of all time including Daredevil (2015), 13 Reasons Why (2017) and Wednesday (2022). The streamer’s top heavy structure, in which the victories subsidize the losses, is nothing new in entertainment. Basic cable was built around flanking one or two hits with cheaper fare. But that’s easier to maintain when you aren’t delivering 891 originals in a given year, as the streamer did in 2022, per What’s On Netflix.

It’s interesting to note that Netflix’s average show demand hit an all time high in January 2017 on the heels of successes such as Fauda Season 1 (Dec. 2, 2016), Fuller House Season 2 (Dec. 9, 2016), One Day at a Time Season 1 (Jan. 6, 2017), A Series of Unfortunate Events Season 1 (Jan. 13, 2017) and more. Its best extended stretch of average show demand came between 2019-2020. (Netflix average demand would again spike in early 2020 as the pandemic elicited a surge of new subscribers and engagement). Of course, this came at a time when Netflix enjoyed fewer challengers in the streaming arena. Plus, the number of originals Netflix produced would continue to grow in the ensuing years, which would inevitably impact average demand score.

In fact, the average demand for Netflix shows has been declining since that spike in 2020, from 2.7x to around 2.0x in 2023. This decline coincides with public comments from Netflix leadership in recent years about stabilizing the content budget. As the company continues to mature and face stiffer competition, it’s no longer about unearthing a game-changing hit every quarter to make up for the caravan of content that goes nowhere. It’s now about focusing original programming spend on what works (Squid Game reality series spinoff!), strategically licensing, and building a library that improves the perceived value of the entire service.

No streaming company wants a reputation for having a junk filled library. As market conditions have forced a reappraisal of loose spending, Netflix has the opportunity to re-emphasize consistent quality to its subscribers.