Price Hikes, Bundles and Syndication: Streaming Reacts To Its New Reality

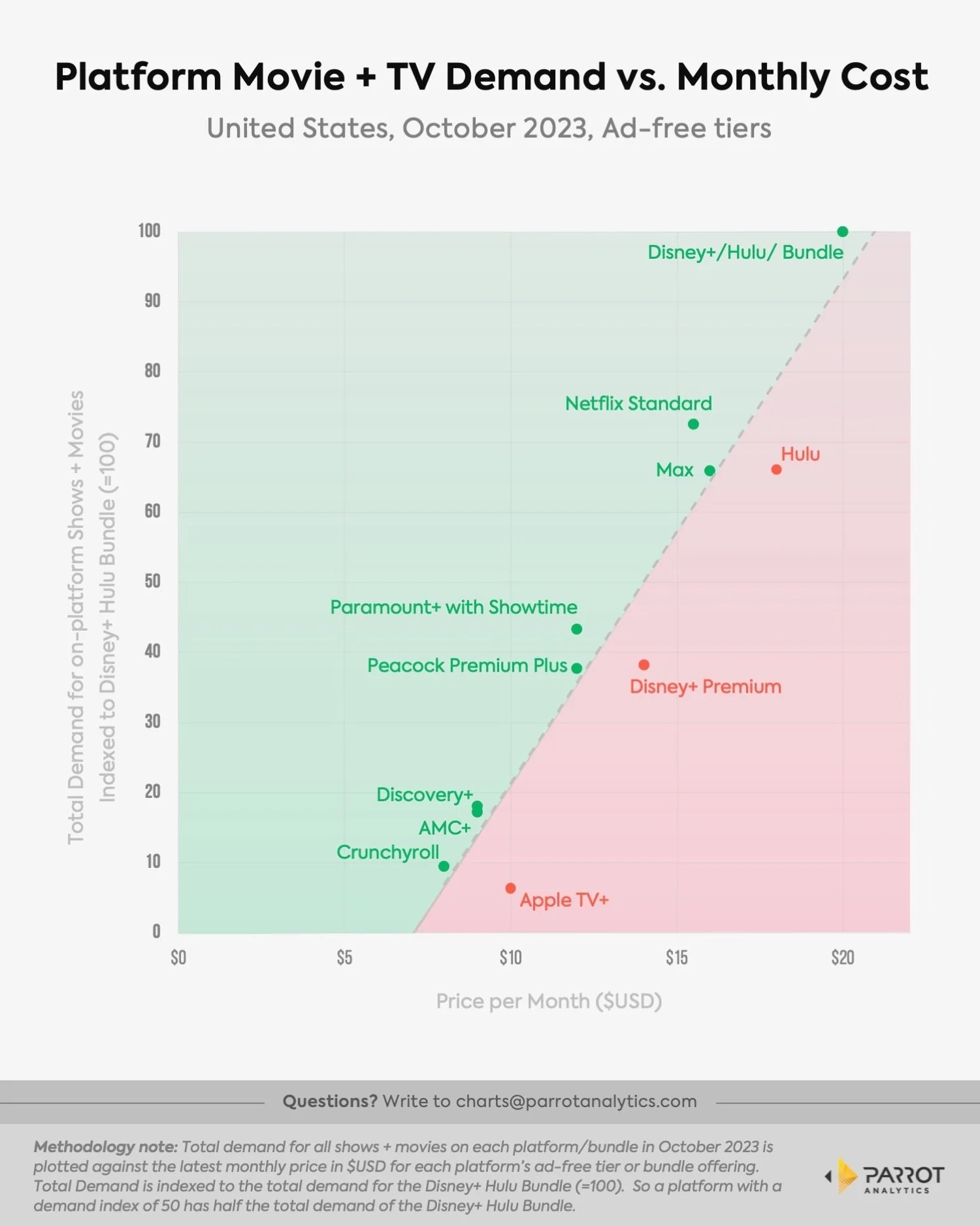

Netflix and the rest of the premium streaming industry have all raised prices over the last 24 months. Increasing the cost of standard and premium tiers, while eliminating basic plans in some instances, is an effort to convince customers to convert to the young and growing ad-supported tiers. At $15.49, Netflix’s standard ad-free package is among the most expensive premium SVOD tiers. There’s no doubt that price hikes will continue to elicit understandable complaints from consumers and, potentially, momentary blips of churn (if not more).

Still, most major services are providing respectable bang-for-their buck when it comes to total catalog demand vs. monthly cost, according to Parrot Analytics data. In other words, the ad-free versions of the Disney bundle, Netflix standard, Max, Paramount+ with Showtime, Peacock Premium Plus and smaller services such as Discovery+, AMC+ and Crunchyroll all remain good values for consumers.

The underlying problem that few are truly addressing is that the only levers available to pull for legacy media in their streaming strategies appear to be library consolidation and price hikes. Paramount+ swallowed up Showtime, HBO Max and Discovery+ merged, and now Disney+ is integrating Hulu. All the while, every major player is raising prices in order to try and leap to profitability rather than experiment with more innovative approaches.

Legacy media can and will continue to seek out bundling opportunities in 2024 and beyond, particularly utility bundles that include added value from non-entertainment services (think Paramount+ and Walmart, the Apple One Bundle, Amazon Prime, etc.). Historically, in addition to locking customers in for a year or more, thus reducing churn, bundles can help with scale and adoption. This then ideally leads to habitual usage and low cost of customer acquisition. Yet bundle pricing is a careful balancing act that deserves extra scrutiny in the search for consistent profitability. Verizon’s bundle of the ad-supported versions of Netflix and Max costs $10, or $7 less than subscribing to each tier individually. Will that help either company with revenue, profit and free cash flow? We will find out.

Since Wall Street’s dramatic 180 on the streaming business model in 2022, the industry has taken steps to essentially recreate the pay-TV bundle via the internet. This includes re-opening the licensing market after years of in-house consolidation (a move comparable to syndication), the acquisition and integration of live events and sports rights (whichare almost single handedly propping up linear television) on streaming, bundling more than one service in a single offering, and more.

But why isn’t the industry rethinking recommendations and discoverability in order to unlock the full value of these combined libraries and train audiences to dip a toe outside of their comfort zones? Why aren’t there overhauls to price planning and tiered access structures to protect against churn, incentivize spending and maximize value? Where are the continued experiments regarding program scheduling, content development and fresh marketing tactics? Are there any development plans that aren’t just stealing strategies from the linear TV model (like Netflix’s long-term bet on gaming)?

Over the first half of 2023, churn among the premium SVODs in the US increased 34.5% year-over-year, per Antenna. This suggests that premium entertainment libraries alone are not enough to consistently secure consumer attention and spend. (No wonder YouTube is lapping the competition). So while the majority of these services remain good value for consumers based on current prices and libraries, that won’t be the case for long if the only changes these companies make is how much customers are being charged.

It’s about evolving the product to meet an array of consumer needs, not just squeezing more money out of your existing customer base.