Media Mergers and Revenue Multiples

For media entrepreneurs running mid-size firms and seeking an acquisition this year, the target exit price is 2–4X revenue. In order to command that multiple, a firm should be focused on a specific content niche and have raised less than $60M in capital.

This thesis is based on two key data points: the market cap to revenue ratios of the largest publicly traded media companies and the middle-market media acquisitions of 2019.

In the current ecosystem, Brat TV and The Information are two companies that fit the ideal M&A profile.

Revenue Multiples

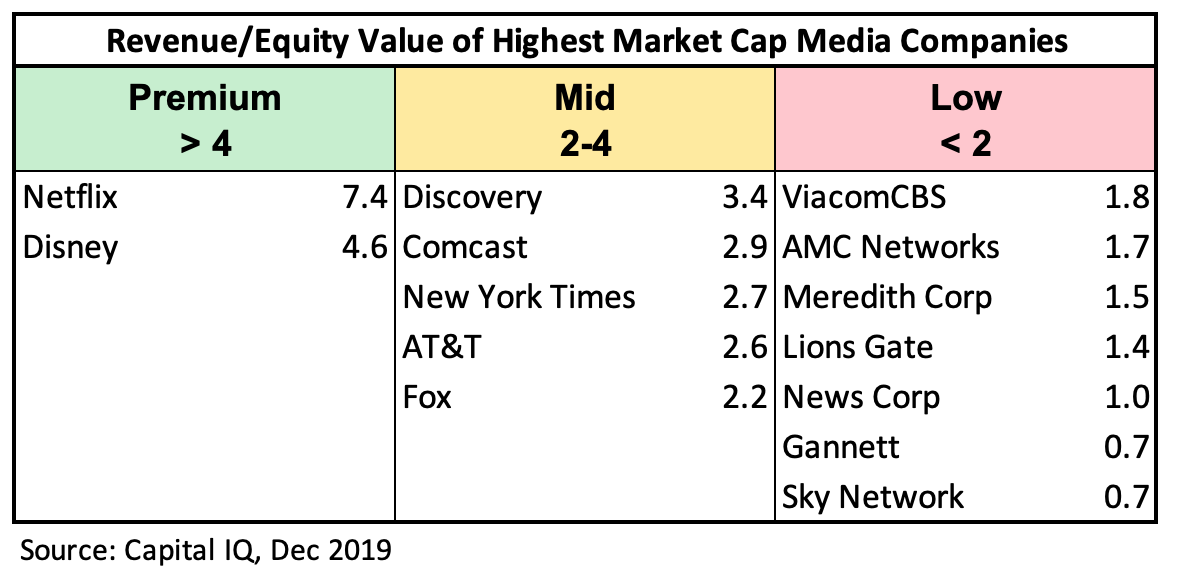

There are only two media stocks that trade above a 4X multiple of revenue: Disney, the most iconic media brand in the world, and Netflix, a company that reshaped the entertainment industry. The best of the rest for video content creation and distribution trade between 1.5 and 3X revenue.

In traditional journalism and publishing, The New York Times leads the pack at a 2.7X multiple after gaining over 1 million subscribers in 2019. The other big newspaper firms, Gannet and News Corp, average a 0.85 multiple -- not a strong sign for the category.

Taken together, these multiples provide guideposts for the exit price an investor or entrepreneur can expect for their media firm.

2019 Acquisitions

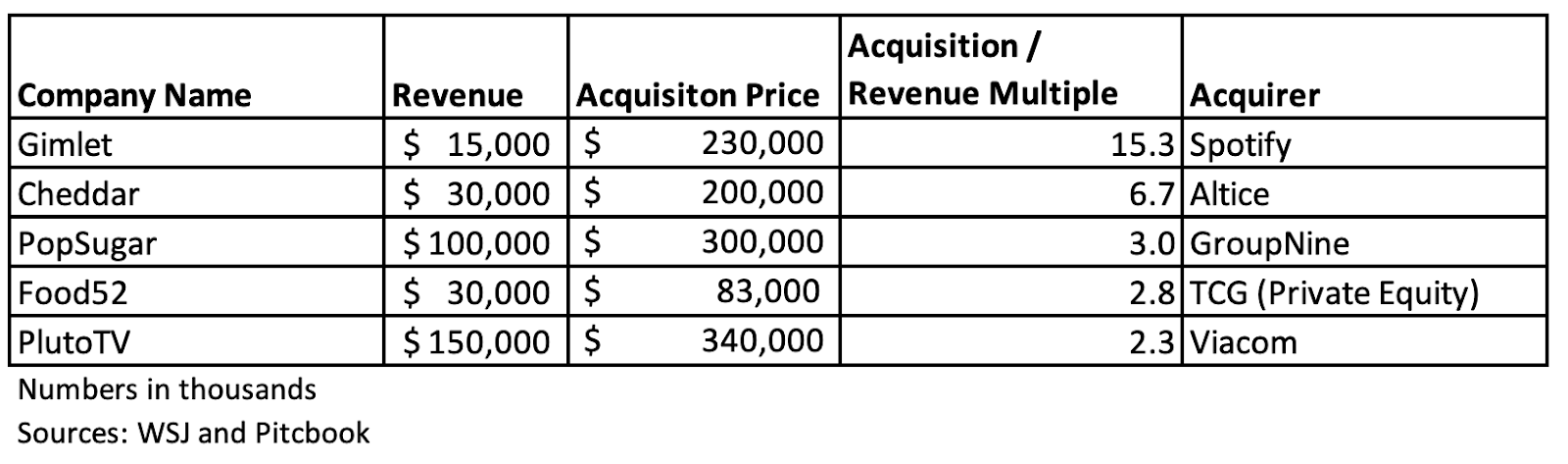

There was significant consolidation in the industry in 2019. While a majority of the attention was focused on big-dollar deals like Disney’s $71 billion purchase of Fox and Viacom’s $15 billion reunion with CBS, there was also considerable movement in the middle of the market - 22 media mergers with a deal value between $15 million and $500 million, according to data from Pitchbook.

Of the 22 M&As, the five above most closely align with the public firms analyzed: consumer-facing brands that are producing and distributing digital content.

Excluding Spotify’s acquisition of Gimlet at a 15X multiple (the spoils of being first into the very buzzy podcast industry), a majority of the remaining deals fall into the target multiple category (2-4X) that’s been established by the public markets.

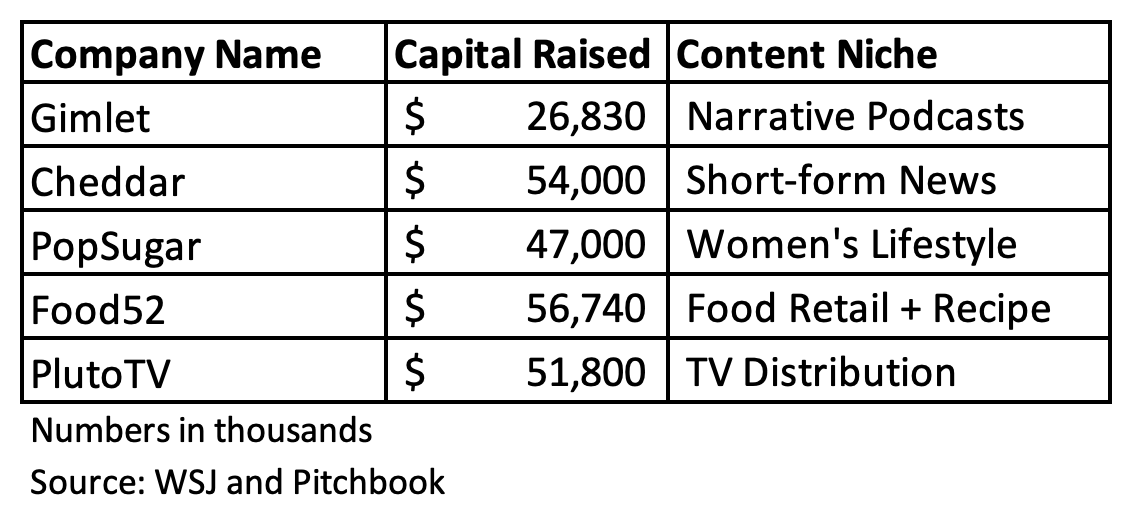

Each of the companies acquired also had two other similarities:

- They focused on a specific content niche (PlutoTV excepted)

- They raised less than $60 million prior to acquisition

Conversely, the M&A market has been light for companies who have raised $100 million or more in capital or have a more diversified content approach. Examples include The Athletic ($140 million raised and exploring a sale, according to the WSJ), Vox ($330 million raised), and Vice ($1.7 billion raised).

2020 Companies to Watch

Industry analysts predict a significantly reduced M&A market for the remainder of the year due to the impacts of coronavirus, increasing the need for firms seeking an exit to fit a specifically attractive profile. These two media brands fit the bill and could command the target 2-4X multiple:

Brat TV

Brat produces scripted television shows aimed at teenage audiences, all airing on YouTube. The company recently shifted away from YouTube’s advertising platform and has hired its own sales staff. Bespoke ads run prior to major new episodes and the company sells sponsored social media posts featuring their talent, driving significant revenue growth.

Brat’s low production costs make it a compelling acquisition target for streamers in need of content. According to Fast Company, the company’s cost of production is $3,500 per minute, while an average TV network spends $25,000 per minute and soon-to-be-launched Quibi spends a staggering $100,000 per minute. As the streaming wars drive up the costs of TV production, advertising based streaming platforms (AVODs) like Peacock, Roku, Pluto or (recently acquired by Fox) Tubi, might look longingly at Brat.

Capital Raised: $42 million

Revenue: $10 million in 2019 and going to $25M in 2020, according to CEO Rob Fishman, via Digiday.

Target Acquisition Price: $100 million or 4X revenue. Brat can expect a premium multiple on revenue because of its 150% year-over-year revenue growth and the competitive nature of the streaming wars.

The Information

Founded in 2013, The Information aims to produce high quality tech-focused journalism. The company has a strict paywall, with its content only available to subscribers who pay $399 per year. The information also has a B2B subscription and an events business.

The outlet’s most popular stories last year included deep-dives on Amazon Web Services and original reporting about sexual harassment allegations against the founder of SaaS unicorn Intercom.

In a recent interview with the New York Times, CEO Jessica Lessin would not confirm a subscriber count, though it’s estimated to be in the ballpark of 300,000. The Athletic, a sports subscription news outlet, has 1M subscribers, but has raised $140 million and is not profitable (in part due to the big salaries they're carrying). The Information, on the other hand, was self-funded by Lessin with under $1M and reached profitability in 2016.

Capital Raised: Sub-$1 million

Revenue: Roughly $12 million, based on subscriber estimates and price, and growing.

Target Acquisition Price: $40 million or 3X revenue. The 2019 acquisitions of Food52 and PopSugar came in at a 3x revenue. The Information’s subscription-based model is appealing, though journalism has not fared well in the public markets.

The above analysis is not meant to suggest that Brat TV and The Information are the only potential media acquisitions this year, or that 2–4X revenue is the only outcome an investor or entrepreneur can expect. The year 2020 has already seen one exception: The Ringer was acquired by Spotify for ~10X revenue multiple in February.

Rather, this framework identifies the type of companies are likely to be acquired and the likely deal value. Case in point: Barstool Sports (sports and comedy focus, $27M raised) was recently acquired by Penn National Gaming at a 4X revenue multiple.